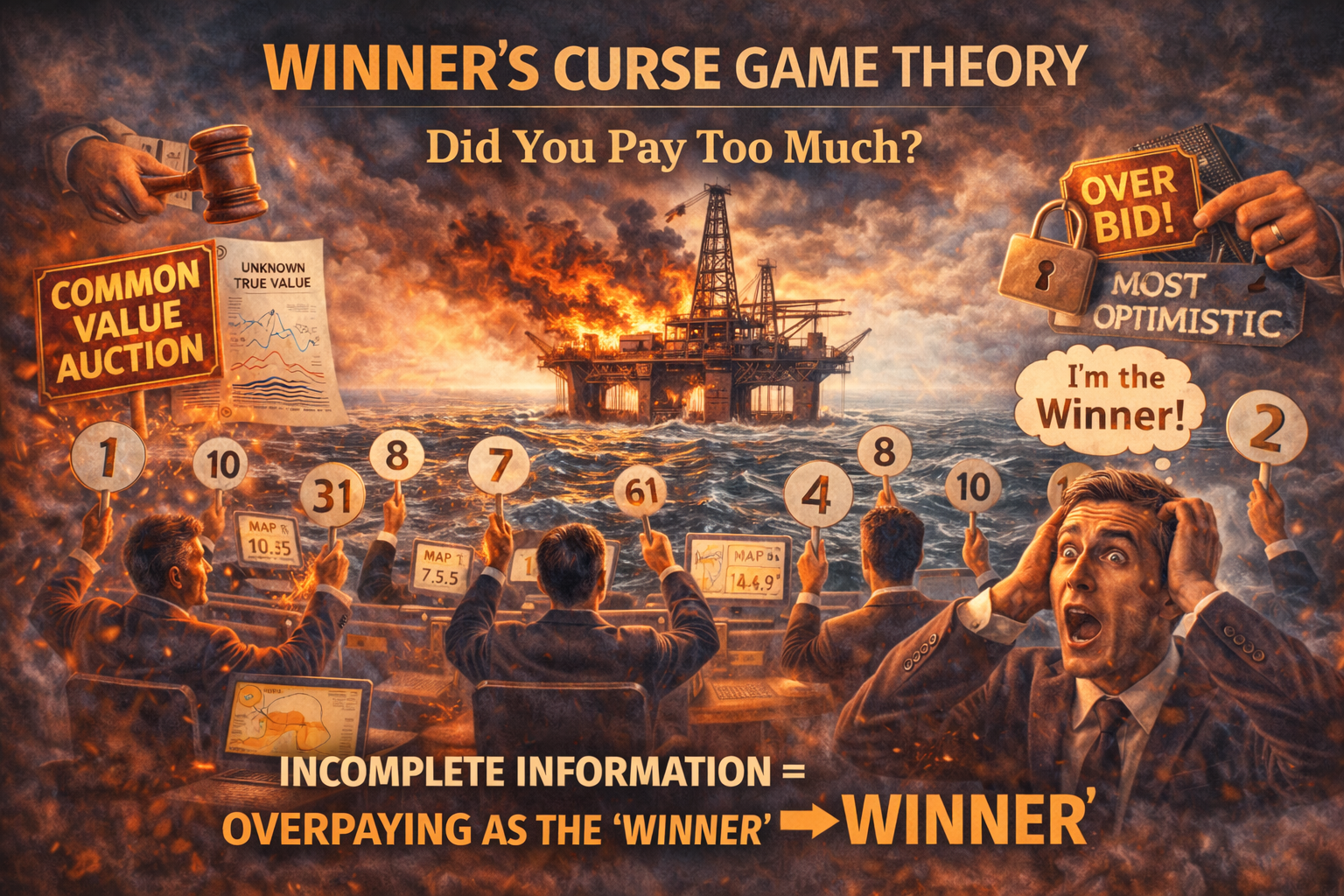

In a “common value” auction—where an item has roughly the same objective value to everyone, but no one knows exactly what that value is—the person who wins the auction is frequently the person who loses the most money. This is known as the Winner’s Curse.

- The Curse

The logic is a statistical trap. Imagine ten oil companies bidding on a single offshore field. Each company conducts its own surveys to estimate how much oil is underground. None of their “maps” are perfect; some understate the value, and some overstate it.

The Trap: The company that submits the highest bid is almost certainly the one that had the most optimistic estimate. If the average estimate of all companies was the “true” value, the winner is the outlier who bid far above that average. They “won” the right to the oil, but they likely paid more than the oil is worth.

Application: This appears in high-stakes mergers or freelance bidding. If you “win” a freelance contract by underbidding every other professional, you haven’t necessarily outsmarted the market. You may have simply been the most “optimistic” (or least informed) about how much work the project would actually require. You won the job, but you lost the profit.

Part 4 Reinforcement: The Reality Check

The Winner’s Curse is a direct consequence of the structural failures we identified in our reality check.

The Information Gap: The Winner’s Curse is entirely a failure of information. If you optimize your strategy based on a “hallucinated” map—whether that’s a faulty geological survey or a misunderstood project brief—you will win the game but lose the payoff. The math of your bid was “rational,” but because your input data was wrong, the output was a disaster.

The Rationality Assumption: We assume that because someone is bidding a lot of money, they must know something we don’t. This is a dangerous projection of rationality. In a high-pressure environment (like a “live” auction or a fast-paced corporate takeover), bidders often fall victim to Bounded Rationality. They get caught up in the “ego” of winning the prize and stop calculating the actual utility of the outcome.

The Complexity Ceiling: In the modern economy, determining the “common value” of an asset (like a tech startup or an AI patent) is nearly impossible. There are too many variables to create a clean payoff matrix. When the complexity is too high, the “curse” becomes more common because the gap between the most optimistic and most pessimistic estimates widens.

Misidentifying the Game: You might think you are in a Common Value Auction (where everyone is trying to find the “true” price), but a competitor might be playing a Predatory Game. They might be bidding an “insanely high” price not because they think the asset is worth it, but because they want to bankrupt you by forcing you to overbid, or they want to keep the asset out of your hands at any cost.

The Key Question

When you “win” a competitive bid, stop celebrating and ask: “What do they know that I don’t?” If you are the only person willing to pay that price, you have to consider the possibility that you aren’t the smartest person in the room—you’re the one with the most broken map.

Strong writing, strong insights, strong utility.

The site continues to be outstanding.